Many home loan customers have expressed great relief at the two recent rate cuts with many now experiencing the lowest interest rate environment they have ever seen. The question you need to ask yourself is how will you use them to your advantage?

According to the Australian Bureau of Statistics (ABS), the average mortgage size in Australia is $384,700 (November 2018). Depending on where you live, this may sound like a lot – or very little – and that’s because the state or capital city you live in has a major influence on the size of your mortgage.

Unfortunately for Sydney house hunters, the average mortgage size in NSW is $462,100. Compare that to Victoria’s average mortgage size of $400,400 and you will see that Sydneysiders indeed pay a premium for their predictable weather patterns and sunny beaches. In fact, Sydney has the biggest average mortgage size in Australia.

Take a trip across the Bass Strait and – all jokes aside – when comparing mortgage sizes, it’s as if you are in another country. Yes, in the land of the Tassie Devil, and in stark comparison to their Victorian neighbours, Tasmanians have the lowest average mortgage sizes in Australia. Tasmania has an average mortgage size of $275,900, almost $200,000 below NSW’s average.

| STATE | Capital City | Avg Mortgage | Avg Mortgage payment (mthly) |

| NSW | Sydney | $462,100 | $2167 |

| VIC | Melbourne | $400,400 | $1820 |

| ACT | Canberra | $404,200 | $1885 |

| QLD | Brisbane | $352.800 | $1517 |

| SA | Adelaide | $300,700 | $2000 |

| WA | Perth | $346,200 | $1419 |

| TAS | Hobart | $275,900 | $2171 |

| NT | Darwin | $305,700 | $2055 |

OPTION 1: Pay the savings into the mortgage account or offset account

To determine how much you can save with a lower interest rate there is an online calculator here which is provided by ASIC moneysmart. Using Sydney as an example and a 2year old loan.

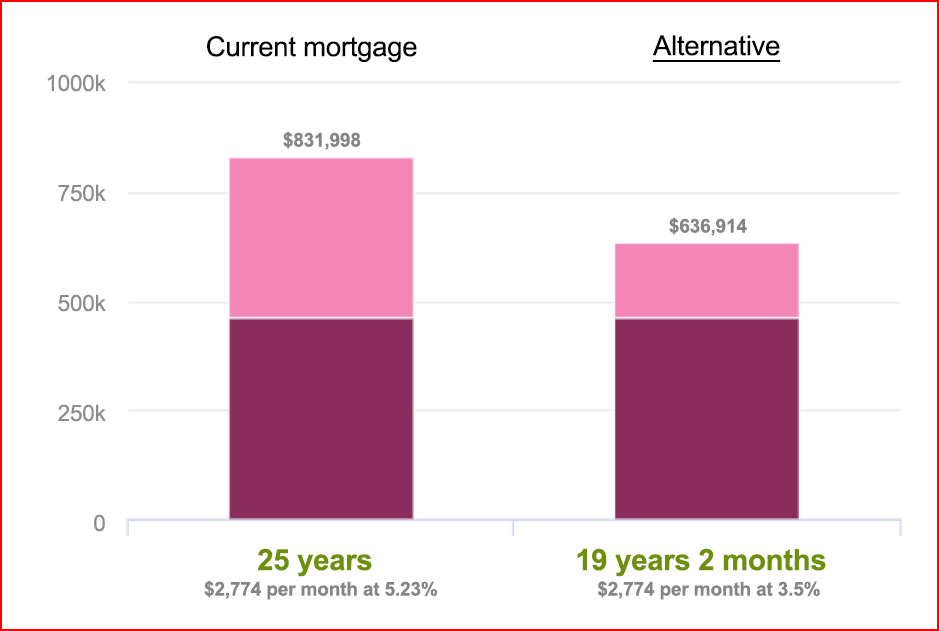

Avg interest rate in Aug 2017 was 5.23% representing a $573/mth reduction for the average Sydney loan

| Mortgage value | Interest rate | Interest rate | Interest rate |

| $462,100 | 5.23% | 4.0% | 3.5% |

| Monthly repayment | $2,774 | $2,449 | $2,201 |

The graph below shows that keeping your payments the same whilst reducing your interest rate from 5.23% to 3.5% will shave 6 years and save almost $200,000 in interest. Imagine the difference if your mortgage is greater than $462,000

Now that’s worth re-financing for!

OPTION 1 alternative: Pay the difference into an offset account

Not all loan products come with an offset facility, but many do, and they are worthwhile having.

Placing the $573 into an offset account means that the balance is deducted from your mortgage balance prior to the calculation of interest. Essentially lowering the interest you pay without affecting the balance. Offset accounts keep you in control of these excess funds and allow you to put them to use elsewhere if needed. Emergency funds, holidays, upgrading household goods, paying lump sums off credit cards or home renovations. The uses are endless, however the key is control. Remember, if you spend what is in the offset, your interest on your mortgage will increase.

OPTION 2: Upgrade whilst the market is low

Traditionally, many Australians have used the market correction to jump a housing bracket.

This is particularly evident with the population who currently live in apartments. They can take advantage of the fact that town homes and free-standing dwellings have fallen back further than apartments in many areas.

Many lenders have followed the notice from APRA with The Australian Prudential Regulation Authority (APRA) proposal suggesting that banks ease lending rules and combined with the rate cuts by the Reserve Bank of Australia, will boost the borrowing capacity of property buyers.

The relaxing of the lending rules and the lowering of this servicing rate from 7% down to 5.5%, provides the borrower with approx. 20% more borrowing power.

Eg; A couple earning a combined $160,000 with 2 dependants can now borrow $841,000 compared to the $719,000 before the changes and interest rate cuts.

That additional amount could be the difference between upgrading or staying put. Additional benefits will be found if the RBA offer a further cut in interest rates in Nov as many are predicting.

So, there you have it, two valuable options available to you today, by capitalising on the current environment of relaxed lending criteria and lower interest rates. It’s never been easier to re-finance to a better loan product, Industry regulators have made it easier to change lenders, removed excessive fees from early payouts and the banks are behaving very competitively.

Whether a re-finance saves you $200,000 or $50,000 we believe it is well worth the time to do so. There is simply no reason not to arrange a mortgage review with a broker.

What do you think?

At Launch Money we believe we offer an indispensable service and hold strongly to the belief that a mortgage broker is the only party to the process who is best positioned to act as an advocate for the borrower.

Our service is more than just securing the lowest mortgage rates, we give you tailored advice to help fast-track your application with the RIGHT LENDER based on your financial goals.

Whether you are buying a new home, personal investment property, commercial property, SMSF investment property, motor vehicle or thinking about refinancing, Launch Money can help secure a better loan and deliver a hassle-free mortgage experience for you.

To speak with a broker at Launch Money call the team on 1300 925 081. Alternatively, you can email your questions to: info@launchmoney.com.au